Managing Card-Based Tip and Gratuity Payments for EMV Chip

Publication Date: March 2017

Executive Summary: The EMV Migration Forum is providing information on how to best manage tips and gratuities as the U.S. migrates to chip, and what options restaurant owners and other merchants in travel and entertainment can pursue. This document is intended to provide a high-level overview of tip processing in EMV chip environment. Please refer to payment network guidelines for specific implementation information.

As the U.S. migrates to chip, certain market segments that accept tips and gratuities via card payments must consider how to best serve their customer base without disrupting current acceptance practices. This is the cornerstone of U.S. chip migration—to ensure continued card acceptance with limited disruption to a merchant’s business.

In the magnetic stripe environment, tips and gratuities paid with payment cards have been handled post authorization, an approach that has largely been accepted by all U.S. stakeholders. This practice does not need to change when chip technology is introduced because processing for post-authorization tips and gratuities is supported for chip-initiated payments. There is nothing particular to chip that would cause a merchant to change this existing practice after migrating to chip.

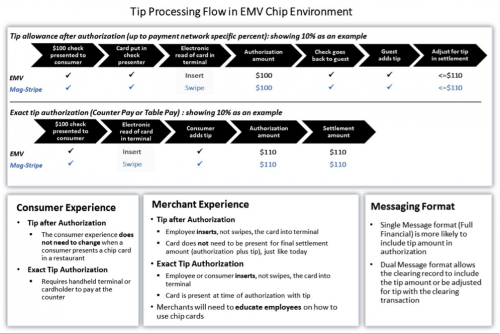

There are three basic acceptance models for card-based tip and gratuity payments, any of which can be adopted for chip acceptance:

- Tip Allowance: This is the predominant practice in the U.S. at table-service restaurants and is suitable for server-station processing of the card-based payment. With this option, merchants authorize for the ticket amount only, excluding tip. A receipt is printed for the cardholder to sign and optionally add a tip at that time. Settlement may be adjusted to include the tip, up to a percent of the authorized amount (payment network specific). If the tip exceeds the network allowance, refer to the payment network processing rules.

- Counter: When paying at the counter, the cardholder may add a tip to their total as part of the checkout process. The cardholder should be advised to follow the prompts on the terminal. The merchant authorizes for the total amount of the transaction including both the ticket amount and the tip amount.

- Table Pay: Using portable terminal solutions the merchant can bring the payment device directly to the cardholder allowing them the opportunity to add a tip amount. The cardholder should be advised to follow the prompts on the terminal. The merchant authorizes for the ticket amount plus the actual amount of the tip.

Note: In the U.S., an authorization request must be for the total amount of the transaction. Unless specifically permitted in the payment network, a U.S. merchant must not use an arbitrary or estimated amount to obtain authorization, and must not add an estimated tip amount to the authorization request beyond the value of goods provided or services rendered, plus any applicable tax.

The three options are illustrated in the diagram below.

Most U.S. merchants recognize the need to deploy a chip terminal to protect against the counterfeit liability shift (from issuer to merchant/acquirer). What may not be clearly understood is that a chip acceptance solution can be added to an existing payment environment without affecting current business practices or approval rates, particularly for market segments accepting tips and gratuities.

If not using the tip allowance after authorization methodology and if a tip is added during a contactless card transaction during Counter Pay or Table Pay, then the consumer must be offered the opportunity to add the tip amount prior to tapping the card.

If it is the merchant’s desire to offer PIN as a Cardholder Verification Method for either credit or debit transactions, then a Counter or Table Pay solution must be considered. In order to enter a PIN, the cardholder must be present at the payment device. The terminal prompts should clearly indicate when to enter tip and when to enter PIN. Note that PIN is not required for chip transactions in the U.S.; therefore, it is not mandatory that a merchant support PIN. Merchants should contact their acquirers for additional information on supporting PIN.

Note: For debit transactions, the acquirer and merchant can continue to determine their preferred routing based on using the U.S. Common AID and editing the candidate list as defined in the EMV Migration Forum white paper, “U.S. Debit EMV Technical Proposal,1” to comply with the Durbin Amendment.

1“U.S. Debit EMV Technical Proposal,” available at http://www.emv-connection.com/u-s-debit-emv-technical-proposal/

Legal Notice

While great effort has been made to ensure that the information in this document is accurate and current, this information does not constitute legal advice and should not be relied on for any legal purpose, whether statutory, regulatory, contractual or otherwise. All warranties of any kind are disclaimed, including all warranties relating to or arising in connection with the use of or reliance on the information set forth herein. Any person that uses or otherwise relies in any manner on the information set forth herein does so at his or her sole risk.

Please note: The information and materials available on this web page (“Information”) is provided solely for convenience and does not constitute legal or technical advice. All representations or warranties, express or implied, are expressly disclaimed, including without limitation, implied warranties of merchantability or fitness for a particular purpose and all warranties regarding accuracy, completeness, adequacy, results, title and non-infringement. All Information is limited to the scenarios, stakeholders and other matters specified, and should be considered in light of applicable laws, regulations, industry rules and requirements, facts, circumstances and other relevant factors. None of the Information should be interpreted or construed to require or promote the establishment of any solution, practice, configuration, rule, requirement or specification inconsistent with applicable legal requirements, any of which requirements may change over time. The U.S. Payments Forum assumes no responsibility to support, maintain or update the Information, regardless of any such change. Use of or reliance on the Information is at the user’s sole risk, and users are strongly encouraged to consult with their respective payment networks, acquirers, processors, vendors and appropriately qualified technical and legal experts prior to all implementation decisions.